Stablecoin regulations are about to take effect, and the Hong Kong market is surging

The stablecoin surge continues to gain momentum.

On one hand, the Stablecoin Genius Act has now been signed into law by Trump; on the other hand, Hong Kong’s stablecoin issuance is entering the final countdown. On August 1, Hong Kong’s “Stablecoin Ordinance” will officially take effect. While the U.S. stablecoin regulations have sent shockwaves through the crypto markets, Hong Kong’s move—though creating only ripples in the digital asset space—has had a rare and outsized impact on the local stock market.

Following the approval of Hong Kong’s stablecoin legislation, the local equity market has seen unprecedented enthusiasm for the sector. Hong Kong’s stablecoin-related stocks have surged dramatically, with multiple names doubling and some soaring more than tenfold. Investors are buzzing and listed companies are enjoying capital inflows. Yet behind this apparent celebration, Hong Kong regulators are voicing new concerns. Recently, Eddie Yue, Chief Executive of the Hong Kong Monetary Authority (HKMA), published an essay titled “Stablecoin: Steady Progress for Long-Term Success,” aiming to calm the overheated market.

But when the market is already at a boil, it’s no easy task to cool things down.

On May 21, the Hong Kong stablecoin bill passed its third reading in the Legislative Council. At the time, with the U.S. stablecoin bill still under Senate review, Hong Kong’s “head start” became a market talking point. In terms of substance—licensing, 100% reserves, HK$25 million paid-up capital, AML requirements—Hong Kong’s rules are in line with leading jurisdictions. But in public perception, attitudes have been polarized, perfectly capturing the volatile reality of stablecoins in Hong Kong.

On one hand, due to Hong Kong’s shrinking influence in crypto and a tendency for headline-grabbing but underwhelming moves, the digital asset market has adopted a cautious, even pessimistic, outlook. Many believe that even with tightened oversight, Hong Kong’s stablecoins will remain little more than an extension of U.S. dollar stablecoins, only marginally relevant in a limited market.

Yet in other markets, the new law was a major boost. Once passed, major enterprises with sharp instincts rushed in, and mainstream media and brokerages spread the news, helping stablecoins break into the broader financial conversation. Debate over the definition, use cases, and significance of stablecoins intensified—and soon expanded to the need for a yuan stablecoin. For the trillion-dollar stablecoin market, it feels like a major inflection point is near.

This Friday, Hong Kong’s stablecoin ordinance will officially come into force, and license applications will open. Yet just one week prior, HKMA’s Eddie Yue addressed the speculative mania with a pointed essay. He emphasized that stablecoins are becoming overhyped and exhibit signs of a bubble. Yue made clear that only a few stablecoin licenses will be issued initially and urged investors to stay rational and independent amid market excitement. HKMA will solicit public comment on both compliance and AML guidelines, and will set more stringent requirements for anti-money laundering to minimize the risk of stablecoins being exploited for illicit finance.

These comments reveal Hong Kong’s anxiety about the state of the market and signal a very cautious approach to license approvals. The reason for such public warnings is simple: stablecoin activity in Hong Kong has become overheated.

The stock market most clearly reflects the bubble. Promising prospects, combined with an industry in its infancy, have turned “stablecoin” into a powerful capital story. Virtually every stablecoin-linked stock has surged, and the impact has been nearly instantaneous.

Guotai Junan International received a securities trading license in June and became the first Chinese brokerage to offer a full suite of virtual asset services. The company soared 198% on June 25. Its year-to-date gain reached 4.58x.

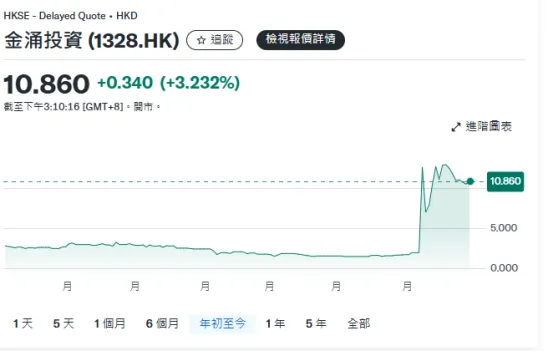

On July 7, Jinyong Investment announced a strategic cooperation framework with AnchorX to jointly explore cross-border payments, trade, and stablecoin adoption across four areas. The very next day, Jinyong shares skyrocketed 533.17% on heavy volume.

On July 15, China Sansan Media disclosed it had begun preparing to apply for a stablecoin license. On July 16, its shares closed up 72.73%, bringing its cumulative gain for the year to an eye-popping 14.95x.

Just a headline can send prices rocketing—evidence of the extraordinary power of the stablecoin narrative. Beyond newcomers, established names such as OKG Technology Holdings, Yunfeng Financial Group, Yixin Group, New Huo Tech Holdings, and OSL Group have each soared over 100% year-to-date. Even China’s much-criticized domestic A-shares have been shaken up, as digital yuan-themed stocks like Hengbao, Sifang Jingchuang, and Chutianlong all logged multipliers in their share prices.

Against this backdrop, every type of company is piling in—trend-chasing opportunists, financial firms looking for a slice of the pie, and strategic giants aiming to lock in lower settlement costs and build competitive moats. As of now, Caixin reports that 50 to 60 companies intend to apply for Hong Kong stablecoin licenses, including mainland China SOEs, financial institutions, and internet giants.

However, a flood of applications does not guarantee that all applicants will receive a license. HKMA has noted that most applicants are stuck at the conceptual level without real use cases, while those with applications often lack the technical or risk management experience needed to issue stablecoins responsibly. Hong Kong wants no part of token issuance for its own sake; this is why HKMA will only grant a handful of licenses in the early phase.

Meanwhile, HKMA is planning a preliminary screening for applicants. According to Caixin, this time the process won’t be standard-form download and mass submissions. Instead, the regulator will pre-screen interested parties through direct communication to assess basic eligibility, and only those who pass the initial vetting will be invited to formally apply.

Who’s most likely to receive a license? Market consensus points to those already participating in the regulatory sandbox program. As early as July last year, HKMA selected JD Chain Technology, CircleLink Innovation, and a Standard Chartered-led consortium (with Adaverse and Hong Kong Telecom) for sandbox testing, now already in stage two. While HKMA stresses that sandbox participation doesn’t guarantee approval, these firms’ prior experience with compliance and risk controls gives them a distinct edge in meeting regulatory expectations.

In summary, Hong Kong’s licensing review focuses on three factors: technical capability to meet issuance requirements; clear use cases and implementation plans; and robust risk controls, especially to combat money laundering. In practice, only large enterprises with proven cross-border finance operations and established risk systems stand a real chance—the playing field for small and medium firms is vanishingly narrow.

At present, despite HKMA’s appeals, FOMO (fear of missing out)-driven speculation is unlikely to cool quickly.

First, Hong Kong’s stablecoin narrative is closely tied to developments in the U.S. With the Genius Act now law, the U.S. stablecoin boom continues, Circle is setting new records, large institutions are showing growing interest, and optimism about rate cuts continues to stoke the market. The hype is likely to remain strong and will continue to spill over into Hong Kong.

Second, discussions around Hong Kong’s stablecoin rulemaking are broadening. Initially, only the Hong Kong dollar stablecoin was in focus, but now attention is shifting to the viability of an offshore yuan stablecoin. National think tanks, local government agencies such as Shanghai SASAC, major brokerages, and industry groups are all weighing in. The prevailing opinion is that a pilot for an offshore RMB stablecoin should begin in Hong Kong, with future experimentation in domestic free trade zones. Previously, slow Web3 development in Hong Kong was blamed on lack of access, but if an offshore RMB stablecoin becomes viable, it could open vast new possibilities—accelerating the sector and having a profound impact on China’s financial system.

Most of all, the stablecoin sector presents lucrative opportunities with a quickly developing industry chain. For retail-focused issuers, stablecoins can sharply cut settlement costs and boost competitiveness. For payment issuers, they offer a gateway to deeper participation in digital asset markets and a path toward global financial infrastructure. Even companies looking simply to ride the hype have reason to play along: amid today’s speculative fever, firms such as ZhongAn Online, Fourth Paradigm, Jia Mi Technology, and Easou Technology have all announced major equity financings. OSL Group is placing more than 101 million shares at HK$14.9 each, raising close to HK$2.4 billion. Beyond issuance, both virtual asset exchanges and bank custodians are racing to tap industry dividends.

In short, hype around stablecoins will remain high in the near term—and with licensing the entry ticket to this compliance race, competition is only set to intensify. But as an early-stage industry, the true reach, spillover, and practical demand for such licenses remain to be seen. With a hard cap of HK$25 million for entry and annual compliance costs likely exceeding HK$1 million, applicants without compelling business models may find themselves worse off for applying. As HKMA noted, only those taking the long view will ultimately succeed—while most hot-money players will be weeded out as the licensing process runs its course.

Investors riding the stock rally should take heed and exercise extra caution.

Disclaimer:

- This article is republished from [Tuoluo Finance]. Copyright belongs to the original author [Tuoluo Finance]. For any concerns about this republication, please contact the Gate Learn team, and we will address them promptly according to established procedures.

- Disclaimer: The views and opinions expressed in this article are solely those of the author and do not constitute investment advice.

- Other language editions of this article are translated by the Gate Learn team. Without explicit mention of Gate, reproduction, distribution, or plagiarism of these translations is prohibited.

Share

Related articles

In-depth Explanation of Yala: Building a Modular DeFi Yield Aggregator with $YU Stablecoin as a Medium

What is Stablecoin?

Top 15 Stablecoins

A Complete Overview of Stablecoin Yield Strategies

What Is USDT0